When I started working at my first full-time job, I had a vague idea of what the Employees Provident Fund (EPF) was, and to be honest, I didn’t think much of it at the time.

The only bit of information that felt significant to me at that point was this: That a good chunk of my salary would be docked and deposited into my spanking new EPF account.

I also knew that I couldn’t touch that cash — or at least most of it — until I turned 55 (the EPF’s currently-defined retirement age) — a milestone that was over three decades away.

And so, my interest in investing was centered only around assets that I could access if I needed to: Stocks, unit trusts and fixed deposits.

When it came to investing in the EPF, I always opted to make the standard, bare minimum contribution. In fact, I barely ever had to think about it since it was all done for me.

Ironically, it was only almost three decades later that I realised what a big mistake that was (I’ll explain why later on), especially once I made FIRE my goal.

But first, let’s get into it:

Employees Provident Fund (EPF): What is it?

Malaysia’s Employee Provident Fund is a statutory retirement savings institution under the Ministry of Finance that’s been tasked with managing the country’s (largely) mandatory pension plan.

Under the Employees Provident Fund Act 1991 (Act 452), any employer, including managers, agents, companies, government bodies and departments that pay a salary of RM10 or more per month to an employee who’s been contracted to provide a service to, or an apprenticeship with them, must pay monthly EPF contributions to the said employee, on the employee’s behalf.

Employees make a mandatory contribution of 11% per month, while employers match this with a 13% contribution to employees who are paid RM5,000 or less, or 12% to employees who are paid more than RM5,000.

In short, once you sign on that dotted line of an employment contract, your employer is legally obligated to contribute to your EPF account at the percentages mentioned above, and so are you.

Who is the EPF for?

As long as you’re a Malaysian citizen or Malaysian permanent resident who’s no older than 75 years (regardless of whether you’re employed or not), you are eligible to open an account with and invest in the EPF.

However, you’re only allowed to contribute as long as you’re 75 or under, so the younger you are when you start, the better.

After you pass the 75-year mark, you can choose to leave your funds with the EPF until you reach 100, and personally, I think this is a smart option for seniors who depend on investment income to fund their lives.

On top of the mandatory contributions from your salary and employer, you can also top up your EPF funds with voluntary contributions by up to RM100,000 per year.

Mandatory EPF contributions, however, don’t apply to: Domestic workers (such as maids, cooks, babysitters, gardeners and drivers for households), employees over 75 years of age, and those being detained in prisons, mental hospitals or rehabilitation centers.

And if you’re freelancer, gig worker, solopreneur or housewife, investing in the EPF would be entirely voluntary, and any self-contributions you make would generally fall under its i-Simpan, i-Saraan, i-Saraan Plus or i-Suri plans.

Alternatively, someone else can fund or ‘top up’ your EPF account for you via the Akaun Persaraan Top-Up Savings or i-Topup plans.

Are your EPF funds safe?

The Malaysian government guarantees your money (and everyone else’s) in the Employees Provident Fund, so yes, it’s safe.

On top of that, the government guarantees a minimum dividend payment of 2.50% of your principal, per year (although its historical returns have been much higher), which literally makes it a high-interest savings account that you can freely withdraw from once you reach 55, or whatever the set retirement age happens to be, if this number gets revised.

The only risk that would lead you (and the rest of us) to potentially lose your money would be if there was a severe (and total) government, currency and economic collapse — highly unlikely, but not impossible.

At this point, we’d all have much bigger problems to worry about than just the EPF.

But as far as low-risk investments go, it can’t get any better than this.

What happens to your money after you contribute to the EPF?

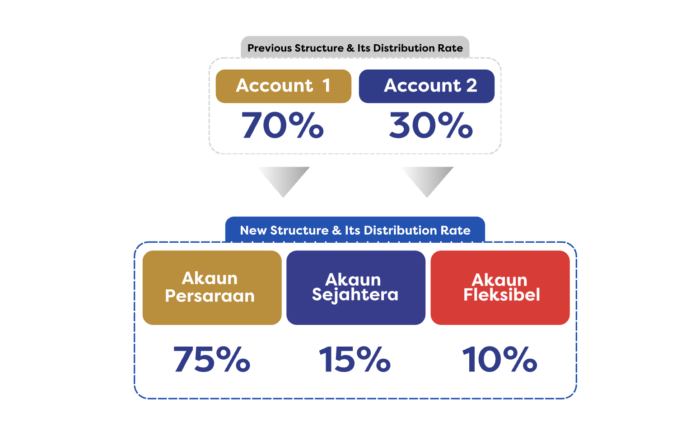

Once the cash from your salary and employer gets deposited into your EPF account, it gets divvied up into three accounts (as of 11 May 2024) by percentage: Akaun Persaraan (75%), Akaun Sejahtera (15%) and Akaun Fleksibel (10%).

If you’d been contributing to the EPF pre-May 2024, your restructured accounts would now look like this:

This means that:

- 75% of your contributions go into Akaun Persaraan, where it cannot be withdrawn because it’s meant to accumulate and compound year after year until you reach retirement age.

- 15% of your contributions go into Akaun Sejahtera, from which you can withdraw funds for what EPF calls ‘pre-retirement’ purposes, such as buying a home, paying for an education, medical expenses, insurance premiums, or a one-off withdrawal once you reach the age of 50, or entirely (along with the rest of your EPF funds) once you hit 55.

- 10% of your contribution goes to Akaun Fleksibel — a recently-added account that, as its name implies, allows you to withdraw from at any time for any reason, with a minimum withdrawal of RM50.

How does the EPF grow your money?

The Employees Provident Fund’s job is to protect your savings and grow it.

To do both, it relies on a portfolio strategy that strikes a balance between stability and growth.

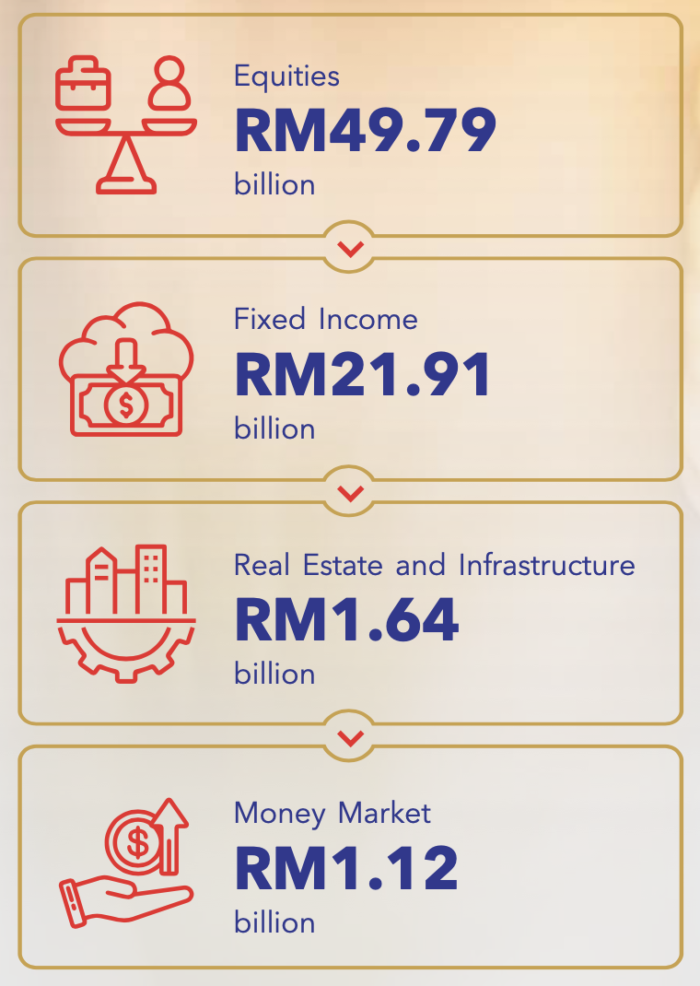

To give you a better idea of what that means, here’s a breakdown of where EPF’s 2024 RM74.46 billion total investment income came from:

As you can see, the biggest driver of returns for its portfolio is domestic and global equities (ie. stocks or shares).

But because of how volatile equities tend to be, the EPF ‘smoothes out’ the ride with fixed income and money market instruments, as well as real estate and infrastructure investments.

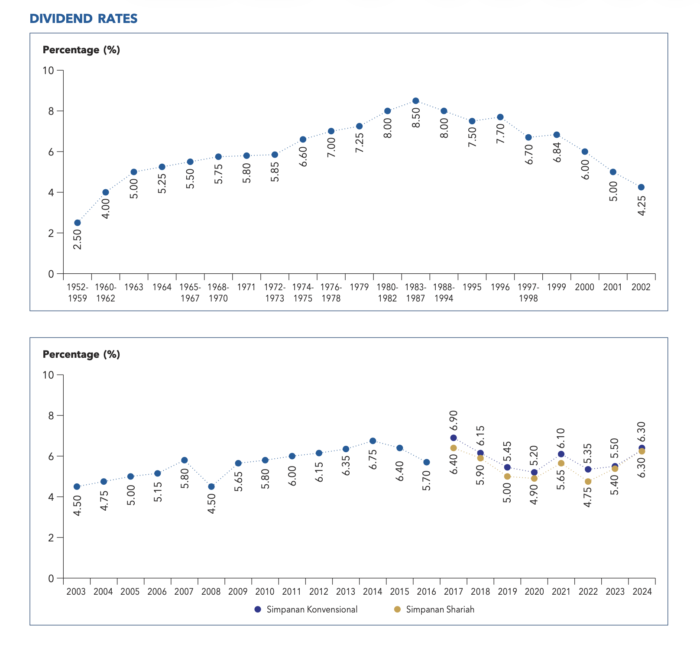

How has the EPF been performing?

The EPF has been delivering above-minimum dividend rates for most of its existence, with payouts tthat have ranged from 5.70% to 6.90% over the last 10 years:

While fixed deposit rates could easily beat EPF’s dividend rates in the 80s and 90s (imagine getting 7-11% interest per year on your principal just for putting your cash in the bank!), this is no longer the case.

These days, just saving your cash gets you a measly 0.20% -0.30% in interest per year, while locking it up in a fixed deposit nets you 2.0%-3.50% at most.

Why should you invest in the EPF?

The biggest gripe I hear when it comes to investing the EPF is this: Accessibility of funds.

Admittedly, this particular ‘negative’ has been one of mine as well, and it has played a role in my not investing more when I was younger.

For me, the gripe is more of a fear of ‘what if?’. What if I want or need to withdraw the money?

Then again, it is meant to be a retirement nest egg (read: Do not touch until you retire), and the EPF has solved this ‘issue’ somewhat with it’s Akaun Fleksibel.

But hey, the benefits (at least for me) of investing in the EPF still outweigh any cons surrounding it:

- It’s one of the most powerful, low-risk investment tools around. The EPF is one of the few investment vehicles that focuses on preserving your capital and delivering a decent annual dividend.

- You get free money. With your employer paying you an additional 13% on top of your salary every single month and your existing balance reaping a 5%-6% dividend each year, you’re literally being given free money just for contributing to the EPF with what feels like little to no risk.

- Zero fees. If you invest via unit trusts, roboadvisors or some other kind of done-for-you investment service, you’d be paying fees of between 0.4% and 5.5% just to get your cash in. After that comes the annual management fees, which can hover around 2.0% for unit trusts and 0.3%-0.8% for roboadvisors. In the long run, these fees will eat into your profits, stunting your portfolio’s growth considerably.

- Contributing gives you tax benefits. Your take-home salary may be taxed, but the chunk of cash that’s deducted and funneled into your EPF account will net you a tax relief of up to RM4,000 per year, while the dividend that’s paid to you every year is fully tax-exempt.

- It 100% automated. Growing your Employees Provident Fund balance is something you barely have to think about since the logistics of how and when your cash gets deposited into your EPF account is taken care of for you. If you’re a self-employed or contract worker, you can recreate this automated setup by having your bank perform a recurring transfer from your savings to your EPF as soon as you get paid each month.

- It’s one of the simplest ways to keep pace with or even beat inflation. With inflation averaging around 2.90%-3.30%, just plonking your cash in the bank and forgetting about it will eventually shrink your future self’s purchasing power, not grow it.

- It takes willpower and resistance out of the investing equation. Personally, this is one of the few instances where I feel like not having a choice works in my favour. Having part of your salary portioned out and deposited into your EPF account for you every single month takes all the resistance out of investing — no willpower or discipline required. This is as good as it gets when it comes to a set-it-and-forget-it way to grow your money.

Is investing in the EPF enough for you to FIRE?

If you’re asking this question right now and are roughly 23 years old and earning at least RM23,028 each month (which adds up to about RM276,336 per year), my answer would be…kind of.

Kind of, as in, yes, provided that:

- You continue to contribute 11% or more of your current earnings to the Employees Provident Fund over the next 22 years or longer.

- The EPF continues to deliver a dividend rate of at least 5.88% (its historical average over the last 10 years, from 2016 to 2025).

- You don’t make any withdrawals from your Akaun Sejahtera or Akaun Fleksibel.

- The government doesn’t change the EPF’s withdrawal policies (like it has in the past couple of years).

- There is no apocalypse, government, currency or economic collapse that would threaten to wipe out your EPF savings.

If you manage to get all these ducks lined up in a row (lucky you!) by 2048, then you’d be all set to FIRE with your EPF balance alone by the time you turn 45.

That is if your annual expenses cost roughly RM76,441 (this works out to about RM6,370 per month) or less per year, which is the amount you’ll earn in dividends from a RM1,300,022 balance in your EPF account, at a dividend rate of 5.88% per year.

For the rest of us who aren’t 23, and don’t have a RM23,000 per month salary in addition to a 22-year investment runway, relying on our EPF balance to FIRE gets a little dicey — there are just too many variables at play here to make it work.

So is the EPF enough for you to FIRE?

My immediate thought is: Not likely.

Yes, make the EPF a part of your portfolio, but it shouldn’t be your only bet when it comes to achieving FIRE, because unless you’ve got a high, five-figure salary coming in every month or are lucky enough to experience a large financial windfall, it’s unlikely that you’ll be able to put enough money into it to reach FIRE.

And even if you do reach your personal FIRE number, it may not necessarily align with the EPF’s withdrawal policies, keeping your funds tied up until you reach its official retirement age anyway.

As you can see, putting all your eggs in the EPF basket to FIRE isn’t just a game of having a long list of variables aligned — it also heightens your concentration risk.

As diversified as it is, having all of your life savings in ONE fund is never a good idea.

How to maximise your EPF returns

Building your Employees Provident Fund war chest is all about slow and steady accumulation.

It’s not fast, and it’s certainly not aggressive.

The magic ingredient at play here? Compound growth.

This means that the best thing you can do to maximise your EPF returns is to:

- Contribute as much as you can, while you can. The younger you are when you start contributing to the EPF (the minimum age is 14, and the maximum is 75), the bigger the head start you have in growing your money. If you’re a salaried employee, you can choose to contribute more than the statutory rate (which currently stands at 11%) via i-Topup, and the maximum amount you can top up voluntarily is currently RM100,000 per year.

- Leave it alone. This means not making any withdrawals for as long as possible. If it brings you any comf0rt, know this: Once your balance reaches the multiple six-figure mark, that’s when it really starts to snowball from year to year.

The role EPF is playing in my own FIRE strategy

Personally, I started ramping up my Employees Provident Fund balance with voluntary contributions only once I entered my 40s.

The reason for this was simple: My 50s suddenly didn’t seem so far away, and I wanted to make the most of the limited runway that was right in front of me.

But as we know, hindsight is always 20/20, and I’ve been feeling a major twinge of regret for not making the most of the longer runway I had in my younger years with voluntary contributions.

In my 20s and 30s, contributing to the EPF was just something I had to do, and beyond checking my account balance once or twice a year, it’s something that I barely thought about.

Now that I’m on the brink of heading into my 50s, the EPF has started to take on a more prominent role in my FIRE strategy (obviously, I’m a little late to the FIRE game), in that I’ll soon be able to use my EPF dividends as another source of passive income.

If I could turn back time (knowing what I know now), here’s what I would do differently:

- Invest with specific goals in mind. Instead of winging it by saving and investing randomly, I would have set a specific FIRE goal to work towards. This way, I would’ve been more motivated to stay consistent and methodical with my overall investment journey. In fact, I probably could have gained clarity much earlier on about the role my EPF savings would play in my retirement, regardless of whether I retired early or not.

- Invest more, voluntarily. Rather than consider those monthly deductions an inconvenience, I would have opened my eyes and seen them for what they were: A safe, zero-cost way to grow my money. And as such, I’d have chosen to put more in, on top of my and my employer’s mandatory contributions, allowing my EPF balance to grow faster.

- Invest with more intention. Taking a deep dive into the EPF’s inner workings, like its investment strategy would have given me the insight I needed to make smarter investment decisions, like how to design the rest of my investment portfolio.

- Focus on earning more, instead of just earning. I’ve shared in a previous post that for over half of my working life, I never negotiated my salary. Big mistake. Instead of going as deep as I could, I went wide….by taking on multiple jobs to earn as much as I could only to end up working myself into a state of chronic burnout. If I’d learned to advocate for myself earlier, I’d have ended up earning more and subsequently contributing more to my Employees Provident Fund balance. And who knows? I might have reached the key milestones in my FIRE journey much, much sooner.

What about you — what’s your EPF strategy and what role will it play in your own FIRE journey? I’d love to know in the comments below.

Recommended Tools & Resources

*Note: Some of these suggestions contain affiliate links, which means that I’ll earn a small fee if you decide to use them. Using these links won’t cost you anything extra, but it’ll allow this blog to earn some money. If you use them, thank you 🙂

StashAway puts my cash to work by diversifying it into baskets of global exchange-traded funds (ETFs) safely and easily according to my risk appetite minus the freakishly high sales and management fees that come with unit trust funds. Sign up here to save 50% on management fees when you invest up to RM100,000 for your first 6 months.

Got financial goals in mind but don’t know how to make them happen? Use the very same step-by-step process I do to give my goals the structure and clarity I need to take them from idea to reality. Get your copy of The ROF Financial Goal Planner here when you sign up for my newsletter.

THE MILLIONAIRE NEXT DOOR by Thomas J. Stanley and William D. Danko

This is the very first book I ever read about money, and one that opened my eyes to what it really means to be wealthy and how the true rich (ie people who have a lot of money and are smart with it) make, manage and use the green stuff. You can get your copy here.

YOUR MONEY OR YOUR LIFE by Vicki Robin

I consider this mandatory reading for everyone, no matter where you are on your financial journey. If you’ve got questions about how to develop good habits around tricky subjects like debt, earning, spending and your relationship with money, this book’s got the answers. You can get your copy here.

THE 4-HOUR WORK WEEK by Timothy Ferriss

This isn’t a personal finance book per se, but it is about making money in ways that have nothing to do with working a 9-5 job and introduced me to the idea of mini retirements. If lifesyle design is your thing, this is a must read. You can get your copy here.

Feature photo: faizzaki/DepositPhotos

Leave a Reply