If you’ve read my previous posts, you’d know that I’ve been investing in unit trust funds for well over a decade.

I’m glad that I started investing early in my working life, but I’ve become increasingly sensitive to how much their fees have been eating into my investment returns regardless of whether the funds perform … or not.

If you’re not familiar unit trust fees, they can go up to 5.5% in initial sales charges plus up to 2.0% in annual management fees.

I’ve been on the lookout for more cost-efficient ways to invest for awhile now, so when I heard that the Singapore-headquartered StashAway was coming to town, I was excited.

I made my first deposit in November 2018 have been invested for just over 7 years now — way past the medium term or 3-5 year period that StashAway recommended I stay invested so that there is sufficient time for my principal to “accrue income”, as they put it — so it’s a good time to check in on how my investments are doing.

But first, let’s jump into some basics on StashAway for context just in case you’re new to it, in which case, you’ll likely have the following questions in mind:

What is StashAway and how will it grow my money?

To put it simply, StashAway is a robo-advisor: An algorithm-based investment tool that typically divvies up your cash and puts them into buckets of global, regional, index and sector-driven exchange-traded funds (ETFs) based on your risk appetite.

Once you deposit your cash in ringgit, StashAway converts it into U.S dollars and does all the ETF buying for you.

And as the term ‘robo-advisor’ suggests, the algorithm-driven platform relies on little to no human supervision to grow your cash, hence the significantly lower fees.

Plus, this also means not having the ups and downs of human emotions (which have been known to lead to not-so-great investment decisions) in the mix.

Convenient? Check. Dollar cost averaging (DCA)-friendly: Check.

But now you’re wondering…

Is StashAway safe?

StashAway is licensed and regulated by the Securities Commission (SC) Malaysia, which means that it’s being run according to the SC’s strict rules and regulations.

When you deposit your cash into StashAway, it first goes into a Citibank trust account before being transferred to a Saxo Capital Markets custodian account, where your cash is then held and traded from.

If you park your cash in StashAway Simple, it’ll be held by HSBC Malaysia Bhd.

In other words, your cash and subsequently, investments, are held separately from the money that’s used to fund the company’s operations so that in the unfortunate event that StashAway goes belly up, its customers’ money is kept separately and untouched from the company’s own assets.

As far as fraud and security breach prevention measures go, StashAway uses two-factor authentication, one-time passwords, withdrawal notifications, and round-the-clock server monitoring in addition to intrusion detection systems to keep your funds and data safe.

So yes, it’s legal and safe (but not without the market and foreign exchange risks that come with investing in global stocks, since ETFs are essentially baskets of such stocks) to use.

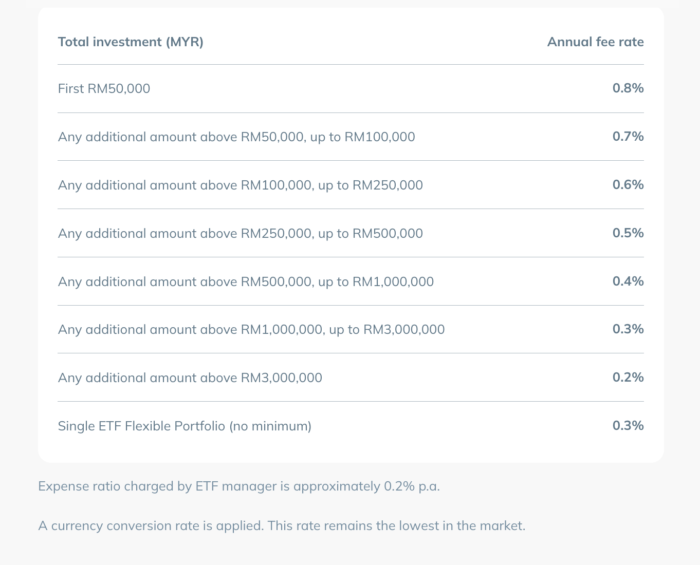

How much will it cost?

The annual fees at StashAway are priced according to a tiered system, which means that the more you invest, the lower your fee rate:

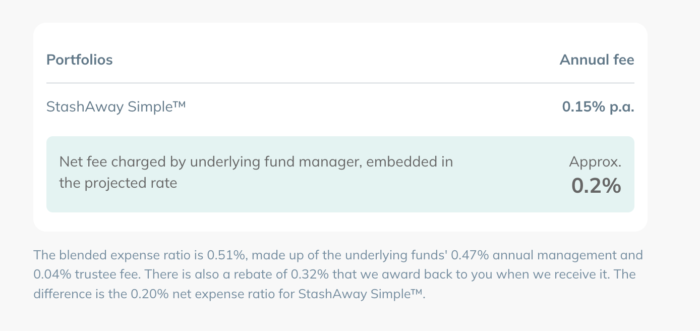

And if you’re using StashAway’s cash management portfolio, StashAway Simple, it’s free, save for the underlying funds’ (Principal Islamic Money Market and AmIncome Funds) 0.15% annual management fee:

However, be aware that the funds that StashAway invests in do charge fees as well, although they tend to be significantly lower than say, unit trust funds, where the ratio typically ranges between 0.5%-2.5% annually).

At StashAway, the approximate expense ratio across its subscribed funds is 0.2% per annum, while its foreign exchange fee is 0.35% per conversion.

Now that we’ve got these basics out of the way, let’s get to the bits you came here for: My returns.

How am I doing?

I made my first deposit in November 2018 and for the most part, had been dollar-cost averaging monthly (with the exception of the first few months of 2020) in addition to making a handful of lump-sum deposits up until late 2021.

I’ve not made any additional deposits since then to see how the portfolios I’ve already invested in pan out.

I started out with two different risk indexes: 14% and 22%, but tweaked both on several occasions to arrive at my current 22% (conservative) and 36% (aggressive) risk index portfolios.

I chose these risk indexes for a couple of reasons:

- I wanted to diversify my investments.

- I wanted to test and compare how each risk index would perform over time.

- I wanted to balance out the risk of both, given how 36% is the most aggressive option that StashAway offers. I went in being ok with taking more risk with 36% since this is only one slice of my overall portfolio, which I would say is largely conservative.

Despite the constant short-term fluctuations (which I expected) and massive dips in March 2020 thanks to the COVID-19 pandemic and China’s subsequent regulatory crackdowns shortly after, both my portfolios have consistently been in the green and have grown healthily since my first deposit.

Here’s the breakdown of both:

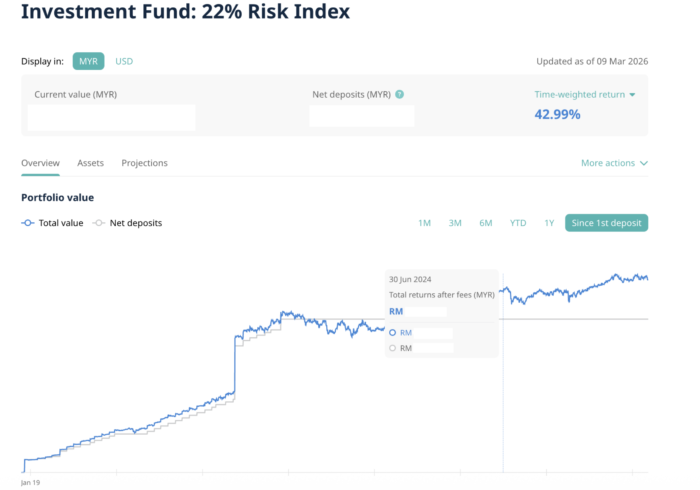

PORTFOLIO 1: 22% Risk Index

Years invested = 7

Time-weighted return = 42.95% (versus 18.65% in 2021)

Money-weighted return = 32.89% (versus 8.33% in 2021)

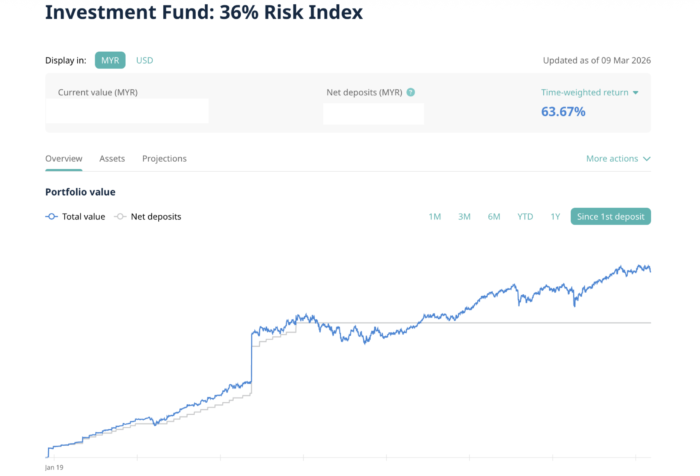

PORTFOLIO 2: 36% Risk Index

Years invested = 7

Time-weighted return = 64.06% (versus 25.44% in 2021)

Money-weighted return = 49.57% (versus 10.69% in 2021)

If you’re wondering what the difference between time- and money-weighted returns are, here’s what they mean:

Time-Weighted Return: This refers to how well StashAway’s portfolio strategy alone performed over time, not taking into account when funds were deposited or withdrawn from it (either as a lump sum or monthly).

Money-Weighted Return: This refers to how well my portfolios performed over the same period, taking into account a host of variables, including whether deposits or withdrawals were made either as a lump sum or monthly, when I made them, and which part of the market cycle I made them at (for example, this is where investing during market highs or lows would make a difference).

You can do a deeper dive into time- and money-weighted returns with StashAway’s explanation of both here.

So for the returns I shared above, the time-weighted returns shows how ShashAway’s portfolio performed over the 7-year period, while the money-weighted return shows how my own investment behaviour affected the returns over the same period.

Back to the numbers: While both portfolios demonstrated strong long-term growth, the 36% risk index portfolio outperformed the 22% risk portfolio, showing very clearly that taking more risk rewarded me with much better returns.

And with both portfolios, my money-weighted returns were significantly lower than StashAway’s time-weighted returns — expected, given how volatile the market has been during this time (and especially after the pandemic broke out).

Most of my gains came after the initial 3 years (when I wrote my first review), telling me that staying invested for the long (I didn’t make any withdrawals over the 7 years) term was the right thing to do.

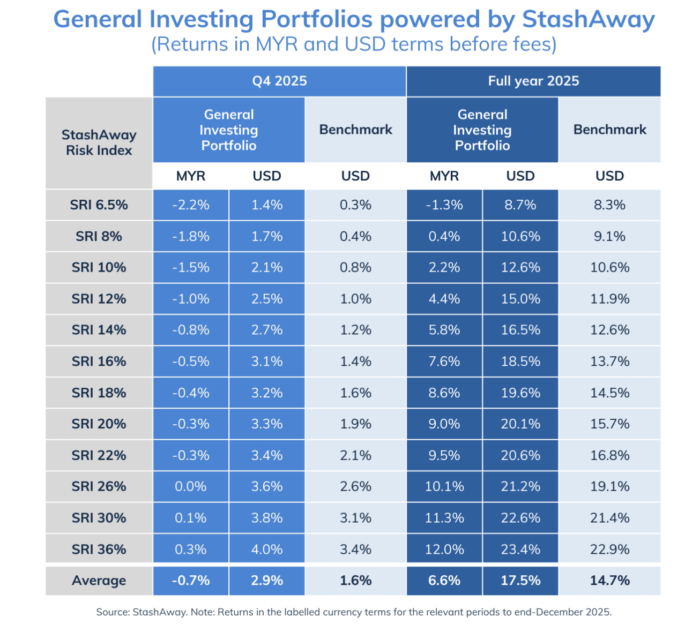

StashAway’s reported 2025 full year returns were 20.6% (in US dollars) for the 22% risk index portfolio and 23.4% for the 36% risk index portfolio — 3.8% and 0.5% higher than their benchmarks (StashAway compares the performance of their funds to that of the FTSE All World Index for equities and the FTSE World Government Bond Index for bonds).

Key Lessons I’ve Learned After 7 Years

Throughout the 7 year period, I did nothing aside from deposit cash into my portfolios.

If I’d done more — like say, made panic withdrawals when the market crashed — I’d probably be swimming in more lessons, and painful ones at that.

Here are the biggest ones that sunk in from my 7-year experiment:

- Time in the market matters more than timing the market: If I had panic sold when COVID hit (like so many people did), I would have turned my paper losses into real ones. Staying invested throughout allowed my portfolios to not only rebound, but gain traction in the years that followed.

- The early years can feel slow or even stagnant: In the first couple of years, it didn’t feel like my portfolios were growing much. Returns only started to snowball past the 2021 mark. This has only strengthened my resolve to trust the process (and the market) instead of giving up on a whim because of how I feel.

- Higher risk results in higher returns: The more risk you take, the more your potential returns. As a largely conservative investor, this is something I’ve always struggled to do, which is why I’ve been taking more steps towards upping my risk in some parts of my overall portfolio.

- Dollar-cost averaging (DCA) affects returns: I lost out on a significant amount of gains in both portfolios because I chose to enter the market at different times (as opposed to investing a lump sum), which means that not all of my funds were exposed to the market from the beginning. Despite this, I’d still DCA if I could start all over again simply because the reality is that I can’t time the market — no one can.

What I like about StashAway

Going into investing with StashAway, I expected affordability and ease of use (I can access the platform on my desktop and through its mobile app), and this is exactly what I got.

This was also my first time investing in ETFs, which is something I’d been wanting to do for awhile.

I also like that:

- Their Flexible Portfolios let you invest in ETFs that track a wide variety of specific assets like gold, silver and copper, or indexes like the Nasdaq-100 or S&P 500. If you’re interested in cryptocurrencies, there are Bitcoin and Ethereum funds to pick from. Looking for Shariah-compliant ETFs or planning to jump on the AI train? You’ve got options.

- I’m able to diversify out of Malaysia without having to take care of the nitty-gritty of offshore ETF investing myself, like foreign exchange, trading fees, buying in fractions, withholding taxes (a portion of which are re-claimed and paid back to investors — something I wouldn’t be able to do on my own).

- They have a transparent, all-inclusive fee structure that costs less (percentage-wise) the more I invest. And obviously, the absence of sales, switching and withdrawal fees are a big plus.

- It’s a 100% hands-off or set-and-forget passive investment vehicle that re-optimises my holdings for me when the economic environment changes, which means that all I have to do is make my deposit (I can also automate this if I wanted to) and focus on living my life.

- I can invest as much or little, and as frequently or infrequently as I like since there are no minimum deposit or lock-in period requirements.

- Their beautifully-designed and easy-to-navigate website and mobile app make accessing my portfolios plus information about their underlying assets, and fund transfers super easy to do.

- They’re constantly evolving and improving. Apart from their done-for-you General Investing Powered by StashAway portfolios, you now also have access to Thematic, Responsible Investing With ESG, Shariah Global, General Investing Powered by BlackRock portfolios.

What I don’t like about StashAway

I’d previously commented that I wished StashAway would offer fully customizable portfolios.

Well, I can now almost check that off my wishlist (read on to find out why), bringing us to my StashAway cons:

Limited portfolio customisation

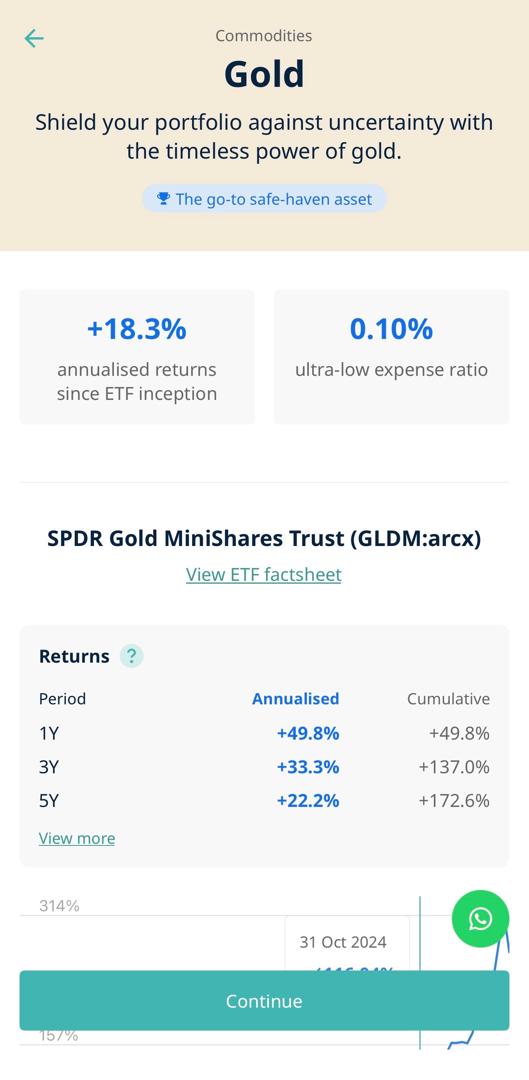

To be fair, this one could be either a plus or negative depending on how you choose to look at it. Yes, you can now choose which underlying asset(s) to invest in with their Flexible Portfolios, but this flexibility has its limits, in that the funds that invest in those assets are chosen for you.

For example, if I wanted to invest in gold, I’d opt to ‘pick my own asset’, and then choose ‘gold’ in StashAway’s ETF Explorer.

But as you can see below, the gold-focused ETF would have already been chosen for me. In this case, it’s the SPDR Gold Minishares Trust.

Likewise for every other asset or index that you opt for.

If you don’t have the time to scope out all the gold-focused ETFs out there or just can’t be bothered to do the research yourself (which would probably be why you’d want to use a Roboadvisor like StashAway), this detail would be a plus.

If you prefer to have more control over which ETF to invest in or are used to DIY-ing it, it may be a deal-breaking limitation.

Fees that (still) compound over time

Let’s face it: Fees are still fees, and fees eat into your profits.

StashAway’s platform fees for its managed portfolios range from 0.2% to 0.8% annually, but there are additional costs that can easily be overlooked — the fee that each individual ETF charges (passively managed ETFs typically charge around 0.2% annually), plus StashAway’s one-time 0.35% foreign exchange fee.

This brings the platform’s annual fee to between 0.4% and 1.0%, plus 0.35% every time you invest or withdraw your funds.

The more you invest, the more these fees add up.

For example, let’s say you invest a RM100,000 lump sum into one of StashAway’s managed portfolios.

That means you’ll pay RM750 a year in platform fees. Throw their 0.35% foreign exchange fee into the mix, and that’s another RM350 when you invest…and another RM350 if you choose to withdraw all your funds.

However, as someone who’s been investing for decades now and explored all kinds of investment products, my perspective is this: Convenience always comes with a price, and sometimes, that price can be a fair trade-off for having someone else do the investing legwork for you.

If you win, they deserve to win too, is how I see it.

Should You Invest in StashAway?

If you’re someone who values:

- Ease-of-use (I have to admit — StashAway’s user interface is beautifully designed, and their thoughtfully curated collection of educational articles and videos on personal finance and investing, very helpful).

- Done-for-you rebalancing, risk management and asset allocation…

…then the fees are worth paying for and StashAway may work for you.

If you’re an investment DIY-er at heart who gets a thrill out of chasing the market and prioritises keeping fees as low as possible to maximise your returns, then StashAway may not be the best fit for you.

Do I plan to keep investing?

Yes, I do, and I’m planning to stay invested for the next 15-20 years at least, as a way to diversify out of Malaysia.

I may consider withdrawing the profits annually to live off once I retire, but seeing how this will disrupt the compounding effect on my funds, I may just leave my portfolios intact for a little while longer before withdrawing my capital plus profits entirely once I start shifting to a more conservative investment approach, or into a drawdown-focused phase of my life.

What role does it play in my overall portfolio?

Right now, I’m looking at my StashAway ‘stash’ as a lower-cost alternative to unit trusts, which I also invest in.

I use unit trust funds as a means of diversifying my portfolio, but as I’ve mentioned before, my biggest pain point with these is the high fees, and so I’m not keen on adding more funds to that department.

Now that I’ve got more data and a positive track record with StashAway to work with, I’m considering trying out more of their other portfolios.

I’ve also been using StashAway Simple as a sinking fund and will probably continue to do so since it’s really easy to use and with a projected (but not guaranteed) return of up to 3.55% per annum, it sure beats keeping my cash in a savings account any day.

Recommended Tools & Resources

*Note: Some of these suggestions contain affiliate links, which means that I’ll earn a small fee if you decide to use them. Using these links won’t cost you anything extra, but it’ll allow this blog to earn some money. If you use them, thank you 🙂

StashAway puts my cash to work by diversifying it into baskets of global exchange-traded funds (ETFs) safely and easily according to my risk appetite minus the freakishly high sales and management fees that come with unit trust funds. Sign up here to save 50% on management fees when you invest up to RM100,000 for your first 6 months.

Got financial goals in mind but don’t know how to make them happen? Use the very same step-by-step process I do to give my goals the structure and clarity I need to take them from idea to reality. Get your copy of The ROF Financial Goal Planner here when you sign up for my newsletter.

THE MILLIONAIRE NEXT DOOR by Thomas J. Stanley and William D. Danko

This is the very first book I ever read about money, and one that opened my eyes to what it really means to be wealthy and how the true rich (ie people who have a lot of money and are smart with it) make, manage and use the green stuff. You can get your copy here.

YOUR MONEY OR YOUR LIFE by Vicki Robin

I consider this mandatory reading for everyone, no matter where you are on your financial journey. If you’ve got questions about how to develop good habits around tricky subjects like debt, earning, spending and your relationship with money, this book’s got the answers. You can get your copy here.

THE 4-HOUR WORK WEEK by Timothy Ferriss

This isn’t a personal finance book per se, but it is about making money in ways that have nothing to do with working a 9-5 job and introduced me to the idea of mini retirements. If lifesyle design is your thing, this is a must read. You can get your copy here.

Get your FREE copy of The ROF Financial Goal Planner and have my latest FI Inspirations and blog posts sent directly to your inbox.

Feature photo: Markus Spiske on Unsplash

Disclaimer: Everything on this blog is published for informational, personal point of view and entertainment purposes only and is not a substitute for professional financial advice. Please consult a certified financial planner for advice on your own situation.

Leave a Reply