I think you’d agree with me when I say that the events of 2020 brought new meaning and urgency to the phrase: “save your money for a rainy day”.

In this case, it didn’t just rain — it poured and hailed with little warning, leaving many of us battered, bruised and struggling with the possibility of not having enough money to live on in the blink of an eye.

While many in my circle had have had to live with massive pay cuts or no job at all as the year unfolded, I’ve been fortunate enough to have been spared from the coronavirus-induced financial chaos, largely due to the saving habits I’d rekindled and nurtured over the past couple of years.

Climbing Out Of A Financial Black Hole

I call the years from 2013 until 2016 a Financial Black Hole because that’s what they were to me: I’d let my financial awareness and health fall to the sidelines (I was literally paying zero attention to it because I was so busy coping with a couple of curveballs life had thrown my way).

This was a time when I had no clue what my money goals were, how much I was spending or where I was going. At the time, it felt like nowhere.

Once I started climbing out of this black hole thanks to a new opportunity and with more peace of mind finally on the horizon, I was able to start saving more money and pick up where I’d left off financially, pre-black hole.

Skyrocketing My Savings

This was also when I discovered the FIRE community and found myself fascinated with how so many people everywhere were going against the ‘work-till-you-drop-until-you-retire’ grain to live life on their own terms.

I wanted in.

Once I got back on my feet, I decided to start off my FIRE journey by tracking every ringgit I earned and spent.

For me, every single ringgit I have has to have a role and purpose in getting me closer to my goal of financial independence and peace of mind, as well as living a work-optional life.

The daily tracking I started doing got me thinking about new ways to save more money.

Initially, my target savings rate was 50% or more, but I was able to get it to 60% or more and recently, over 70%, thanks to (unfortunately) to the coronavirus lockdowns.

Here’s what I’ve been doing over the years to help me get this rate as high as it’s been:

SAVE-MORE-MONEY STRATEGY #1: I Pay Myself First

Once my salary is in, the first thing I do is funnel chunks of it into my investment accounts.

What’s left after my investments are taken care of is what I consider my discretionary spending money — money I give myself permission to spend on anything I want.

Even then, I often end up saving or investing it anyway.

SAVE-MORE-MONEY STRATEGY #2: I Prioritise Earning More

I started investing in dividend-paying stocks in 2008 and have been buying more over the past couple for years to grow my monthly income from these, in addition to my existing unit trust equity and bond funds, fixed deposits and alternative investments like peer-to-peer lending.

Apart from growing my investment income, I’ve also started getting better at negotiating my salary over the past couple of years, and this alone resulted in a 53% pay bump in less than 2 years.

TIP: It’s a lot easier to negotiate a higher salary before you start a new job, so if you have the experience and results to back up your worth, stand your ground while talking numbers!

A huge upside of earning more from multiple streams of income is that the more I’m cash I’m able to bring in, the more I’m able to spend (within reason, of course) without my having my savings rate take a hit.

SAVE-MORE-MONEY STRATEGY #3: I Stopped Shopping For Fun

It’s embarrassing to admit, but shopping used to be something I did A LOT of, especially when I was bored.

That is until the day I decided to spring clean my home and found myself throwing out a ton of things I’d bought on a whim but never used. It was painful to realise that all that stuff I was throwing out used to be money I could have grown into MORE money.

These days, I buy on a ‘needs’ basis with a handful of ‘wants’ throughout the year so I don’t feel deprived.

SAVE-MORE-MONEY STRATEGY #4: I Found A Job Near My Home

I’ve wasted my fair share of time in traffic jams getting to and from work over the years. This is something I no longer want to do.

Luckily for me, I managed to find a gig close to my home. It’s a 4-minute drive to and from the office, but I could walk there in 20 minutes or less if I wanted to.

Despite choosing to drive most of the time (to avoid the heat, rain and lack of pedestrian paths), I’m still saving A TON of cash on petrol and public transportation fees.

To me, this is the ultimate full-time job hack besides scoring a 100% work-from-home role.

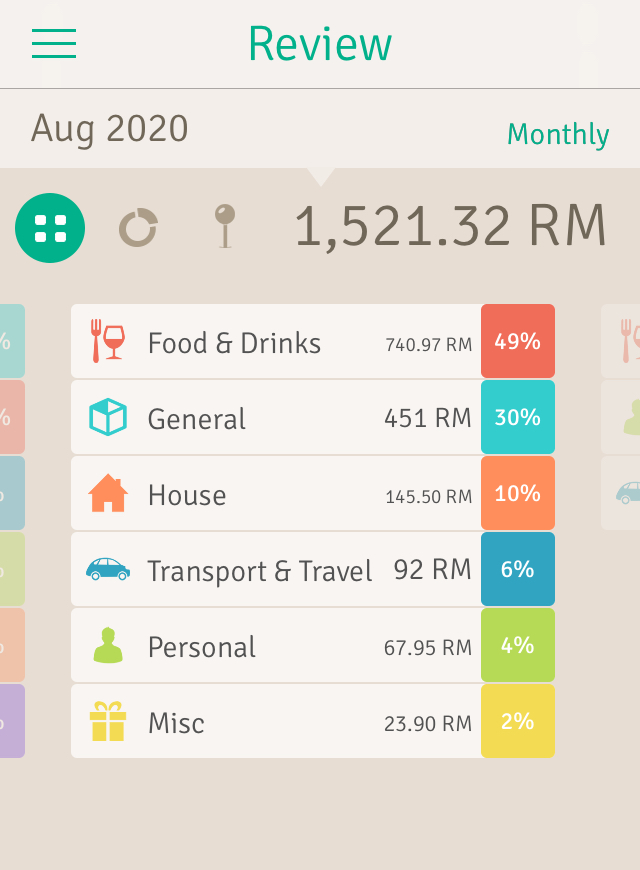

SAVE-MORE-MONEY STRATEGY #5: I Stick To A Monthly Budget

Tracking my cash movement (all incoming and outgoing) has allowed me to not only see how much money I’m earning from all my revenue sources, but also what I’m spending it on, how much and when.

All this hard data on my money habits has been absolutely gold when the time came for me to set my monthly and annual budgets, as well as projections for my 3-year emergency fund/cash buffer.

Now that I know what my numbers and ‘margins’ are, I’m not too fussed if I go over-budget for my monthly expenses, as long it’s within my overall projected range and I’m already saving over 50% of my income.

SAVE-MORE-MONEY STRATEGY #6: I Cook My Own Meals Most Of The Time

I have to admit that this one’s more about personal preference and less about cost.

I could very well head out to get myself a plate of chap fan for under RM7 when week-day lunch times roll around, but I like knowing what I’m going to be eating ahead of time, so I’ll batch cook a dish or two on Sundays that I can just grab and go before I head to work.

I also know myself well enough to predict that eating out will likely involve a restaurant meal that will cost way more than RM25, so it’s better that I venture into the week prepared with my own food.

SAVE-MORE-MONEY STRATEGY #7: I Don’t Use Fancy Skincare Products

For a long time, I thought that the more expensive a beauty product, the more effective it was.

Until I got the opportunity to test just about every product on the market as a beauty writer and realised that they weren’t.

Yes, I still splurge on one or two specific bath products that I love because of their scent and texture, but I no longer buy my moisturisers, serums and sunscreens based on brand.

These days, I buy by ingredient instead and judging by the improvement I’ve seen in my skin over the years, this is something I plan to keep doing indefinitely.

SAVE-MORE-MONEY STRATEGY #8: I’m Learning To Be A Minimalist

No, I’m not planning to fit all my worldly possessions into a backpack, but I do want to live with as little excess as possible so I don’t feel weighed down by stuff I own but hardly use.

The specifics of what this means and how I’m going to get there is still something I’m figuring out, but to start with, I’m doing my best to be more purposeful and intentional about the things I buy.

This automatically translates to fewer impulsive purchases and a healthier bank account balance.

SAVE-MORE-MONEY STRATEGY #9: I Drive An Old Car

I’ve been driving the same car for the past 20 years because my goal with cars has been simple: I have none.

I service my ride regularly to keep maintenance costs down and keep it in the best condition I can, but otherwise, I see cars purely as a means of getting from A to B, so the thought of plonking down anything more than RM70,000 on a new set of wheels feels like a waste of money that could otherwise be invested.

With that said, I do plan to get a new car that’s safer and more comfortable to last me through the next 20 years…paid for in full, in cash.

SAVE-MORE-MONEY STRATEGY #10: I Live With My Family

Seeing how rental and home loan payments easily take the biggest bite out of our living expenses, it’s not surprising that this living arrangement plays a huge role in making my high savings rate possible.

I live in a multiple-generation, multiple-family, and multiple-income household where everyone chips in for our food, utilities and maintenance costs.

Do I wish I had my own space? Yes. Do I want to own a home eventually? I’d say I’m leaning towards a “yes”. But for now, this living arrangement suits me and my family perfectly fine.

Recommended Tools & Resources

*Note: Some of these suggestions contain affiliate links, which means that I’ll earn a small fee if you decide to use them. Using these links won’t cost you anything extra, but it’ll allow this blog to earn some money. If you use them, thank you 🙂

StashAway puts my cash to work by diversifying it into baskets of global exchange-traded funds (ETFs) safely and easily according to my risk appetite minus the freakishly high sales and management fees that come with unit trust funds. Sign up here to save 50% on management fees when you invest up to RM100,000 for your first 6 months.

Got financial goals in mind but don’t know how to make them happen? Use the very same step-by-step process I do to give my goals the structure and clarity I need to take them from idea to reality. Get your copy of The ROF Financial Goal Planner here when you sign up for my newsletter.

THE MILLIONAIRE NEXT DOOR by Thomas J. Stanley and William D. Danko

This is the very first book I ever read about money, and one that opened my eyes to what it really means to be wealthy and how the true rich (ie people who have a lot of money and are smart with it) make, manage and use the green stuff. You can get your copy here.

YOUR MONEY OR YOUR LIFE by Vicki Robin

I consider this mandatory reading for everyone, no matter where you are on your financial journey. If you’ve got questions about how to develop good habits around tricky subjects like debt, earning, spending and your relationship with money, this book’s got the answers. You can get your copy here.

THE 4-HOUR WORK WEEK by Timothy Ferriss

This isn’t a personal finance book per se, but it is about making money in ways that have nothing to do with working a 9-5 job and introduced me to the idea of mini retirements. If lifesyle design is your thing, this is a must read. You can get your copy here.

Get your FREE copy of The ROF Financial Goal Planner and have my latest FI Inspirations and blog posts sent directly to your inbox.

Leave a Reply